Sea-Intelligence estimates recovery to take 8-9 months

While Covid is now entering an endemic phase, supply chain problems continue to plague the industry.

February 10, 2022: While Covid is now entering an endemic phase, supply chain problems continue to plague the industry.

As per an analysis by Sea-Intelligence, return to pre-pandemic normality would take about 8-9 months based on the closest historical event to affect the maritime trade.

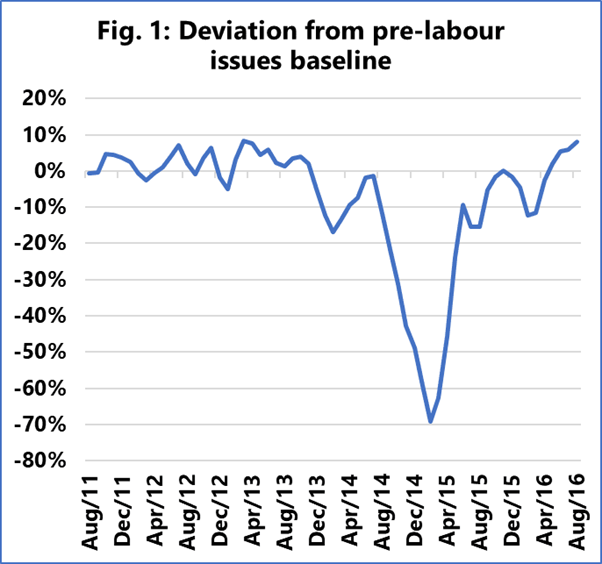

"One element can be used to create a realistic baseline, and that is the US West Coast labour dispute of early 2015, which led to major delays and bottlenecks," says Alan Murphy, CEO, Sea-Intelligence. "We define the period from August 2011 to July 2014 as the pre-labour dispute period and calculate the average baseline reliability on Asia-North America West Coast (NAWC). We then calculate the monthly deviation from this baseline.

"As can be seen in Figure 1, the peak impact of the labour dispute was felt in February 2015 with reliability 70 percentage points below the baseline. Following the resolution of the dispute on February 20, it took 8-9 months for reliability to get back to the baseline. Even when we adjust for the seasonal impact of Chinese New Year, there is no material difference to the picture."

(Credit: Sea-Intelligence)

The schedule reliability on the Asia-NAWC is now just 10.1 percent, which is not markedly different from the 12.6 percent recorded in February 2015, suggesting a return to pre-pandemic normality would also be 8-9 months.

Vessel delays, however, are much worse now (15.07 days) than in 2015 (11.88 days). "As the 2015 problem was resolved in 6-7 months, this means an average reduction in excess delay of 1.25-1.46 days per month. If the current port and hinterland system manages the same speed of recovery this time, the delays also suggest that resolution would take 8-9 months. That said, the market is showing no indication that we have started on the path to resolution."

Freight story is the same

Drewry’s composite World Container Index decreased marginally to $9,359.10/40ft container this week.

While freight rates on the Shanghai–New York route increased 2 percent to $13,437/FEU, rates on the Shanghai–Los Angeles route fell 1% to $10,437/40ft container.

Drewry expects rates to remain stable in the coming week.

Shippers expecting relief in spot freight rates, as traditionally occurs around the New Year, have been left disappointed.

"Another year of Covid impacted Lunar New Year’s celebrations, and a backlog of boxes waiting for exports in the Far East mean little respite for the hard-pressed market," Xeneta wrote in its weekly update.

Rates for containers going into the U.S. have increased since the middle of January, up to $382/FEU going to the West Coast and $603 for the East Coast since the latter continues to prove an attractive alternative to shippers looking to avoid the West Coast congestion.

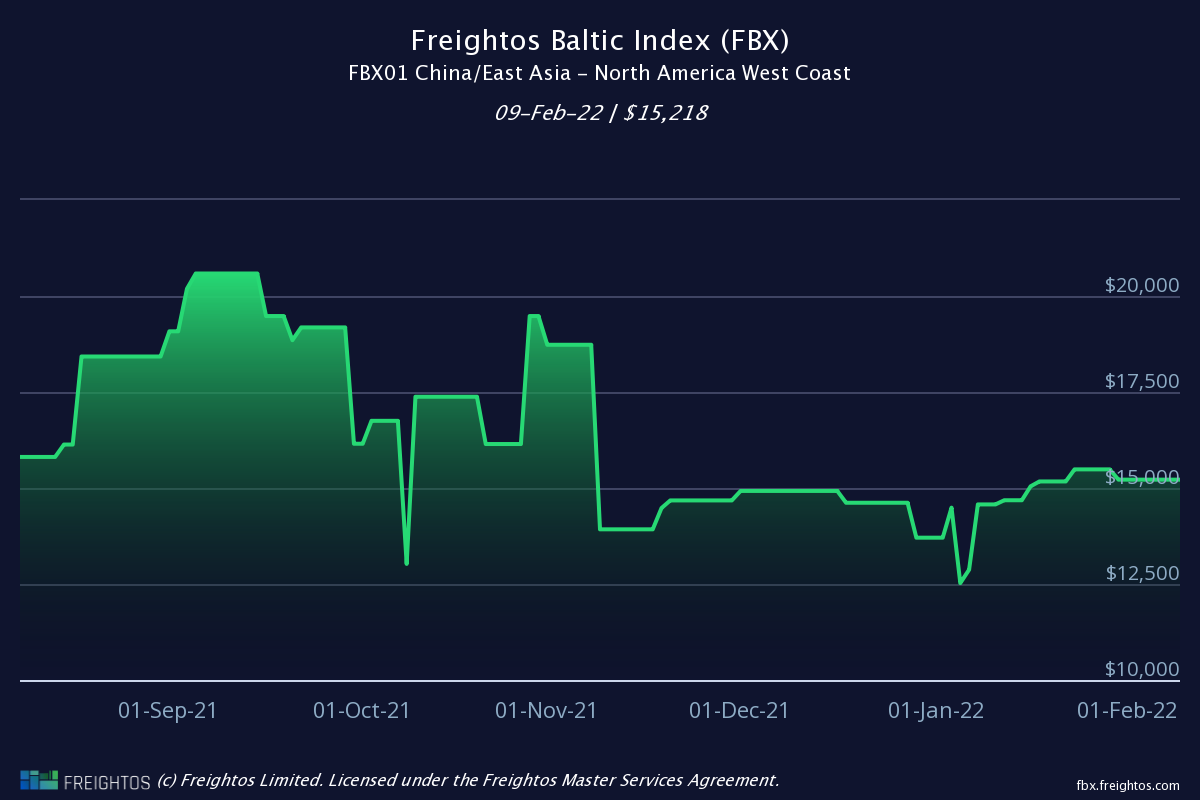

As many as 78 container ships were backed up across the Los Angeles/Long Beach ports as on February 9, a drop of 31 ships compared to the high of 109 touched on January 9, according to data from Captain J. Kipling (Kip) Louttit, Executive Director, Marine Exchange of Southern California & Vessel Traffic Service Los Angeles and Long Beach San Pedro, CA.

Asia-US West Coast prices were steady at $15,218/FEU as on February 9, according to data from Freightos. The rate is 182 percent higher than the same time last year.

Asia-US East Coast prices were unchanged at $16,638/FEU, and are 203 percent higher than rates last year.

Expectations are that rates won't increase significantly just after LNY.

"Along with stable rates, the number of ships waiting for a spot at LA/Long Beach has fallen nearly 30% since early January to fewer than 80 vessels. Though the backlog is still daunting, this development is a welcome first hint of recovery from disruptions that have impacted US importers and exporters."