Earnings of rated shipping companies to fall 17% in 2020: Moody’s

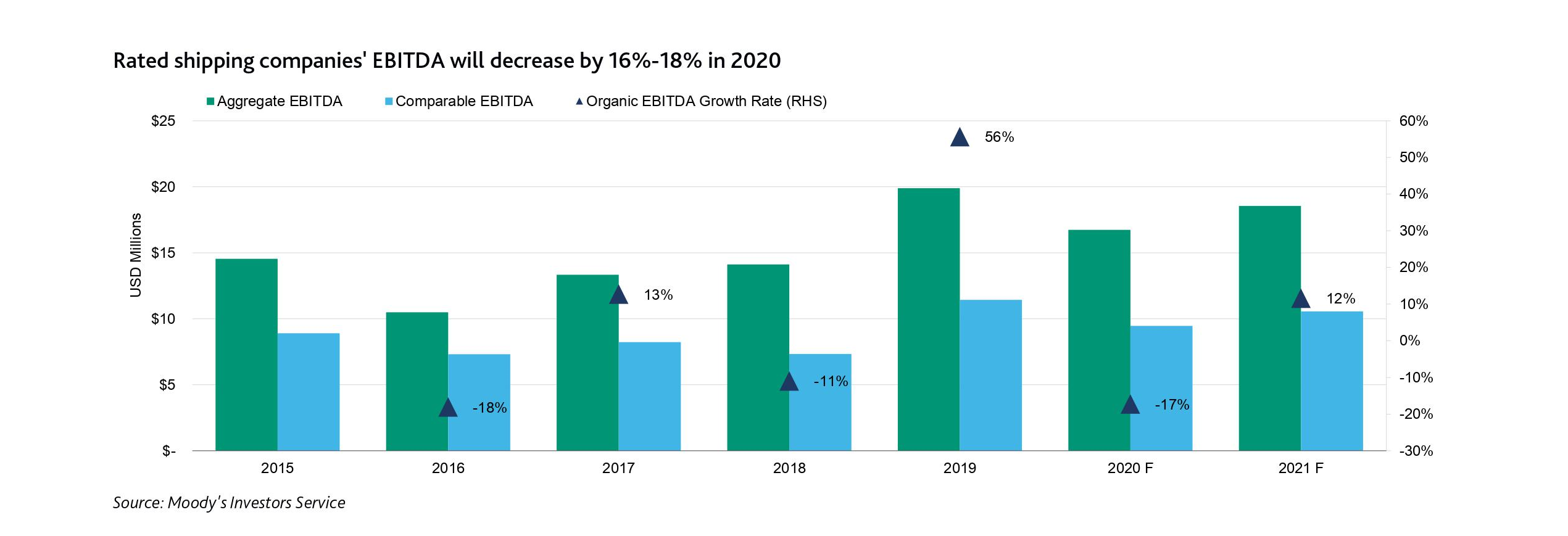

July 13, 2020: Moody’s Investor Service in its latest report on global shipping industry expects the aggregate EBITDA of rated shipping companies to fall by around 16-18 percent in 2020, widening from its previous projection of a drop of around 6-10 percent in March as demand contraction worsens.

The global shipping industry is facing geopolitical uncertainties such as the US-China trade negotiations and the US-EU discussions.

The global shipping industry is facing geopolitical uncertainties such as the US-China trade negotiations and the US-EU discussions.

July 13, 2020: Moody’s Investor Service in its latest report on global shipping industry expects the aggregate EBITDA of rated shipping companies to fall by around 16-18 percent in 2020, widening from its previous projection of a drop of around 6-10 percent in March as demand contraction worsens.

“We expect the global economy to shrink in 2020 and its recovery to be long and bumpy. We think that supply is likely to exceed demand significantly in the dry bulk and container segments with tankers helped by a temporary dislocation in the oil market. Our outlook for the global shipping industry has been negative since March 2020,” said the report.

Challenges

The global shipping industry is facing a number of challenges over the next 12-18 months, including geopolitical uncertainties, such as the US-China trade negotiations and the US-EU discussions. Although the introduction of the International Maritime Organization's lower global sulphur cap on marine fuels (IMO 2020) from 1 January caused less disruption than we expected in the first quarter of 2020 in part because of the recent sharp decline in crude oil prices, the effects of this legislation are still filtering through.

Container segment

Outlook for the container shipping segment remains negative. However, positive signs are emerging following unprecedented capacity adjustments by the carriers, keeping freight rates above last year’s levels despite a significant decrease in the bunker price. Nevertheless, this positive development could be challenged by a resurgence in infections, endangering fragile demand for finished and semi-finished goods in advanced economies in North America and Europe.

Bulk segment

Outlook for the dry bulk segment is negative. Although the sharp decline in the Baltic Dry Index (BDI), a measure of dry-bulk rates, has recently reversed, market conditions will continue to be highly volatile.

Tanker segment

Outlook for the tanker segment is stable. Tanker rates have benefitted tremendously from the high demand for floating storage, but charter rates will return closer to long-run averages in the second half of the year as broad economic weakness finds its way into the tanker market. Positively, new vessel deliveries are reducing in 2020 after several years of overbuilding in the industry.

What would change outlook

“We would consider revising the outlook to stable if both the oversupply of vessels declines materially such that shipping supply growth does not exceed demand growth by more than 2 percent and year-over-year aggregate EBITDA growth appears likely to be between -5 and +10 percent. We would consider revising the outlook to positive if the oversupply of vessels declines materially and aggregate year-over-year EBITDA growth appears likely to exceed 10 percent,” said the release.