Hidden trends in Indian commercial vehicle sales of H1 2020-21

The automotive industry has largely recovered from the lows of the Covid-19 pandemic. However, commercial vehicle (CV) segment has unfortunately lagged behind other segments. Kaushik Narayan of Leaptrucks brings you a detailed analysis of the segmental performance of the CV industry and highlights the hidden trends in commercial vehicle sales in H1 2020-21

The automotive industry has largely recovered from the lows of the Covid-19 pandemic. However, commercial vehicle (CV) segment has unfortunately lagged behind other segments. Kaushik Narayan of Leaptrucks brings you a detailed analysis of the segmental performance of the CV industry and highlights the Hidden trends in commercial vehicle sales in H1 2020-21.

Overall CV industry performance in H1 2020

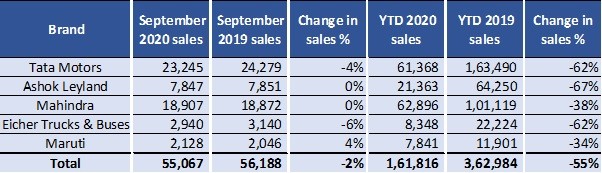

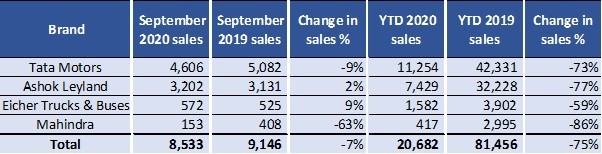

September has been a bright spot in the CV industry. For the first time in 2020-21, the industry performance was almost on par with last year. All major manufacturers performed well in September. However, the industry ended H1 55 percent lower than the same period last year.

Commercial vehicles sales summary for September 2020 & H1 2020-21

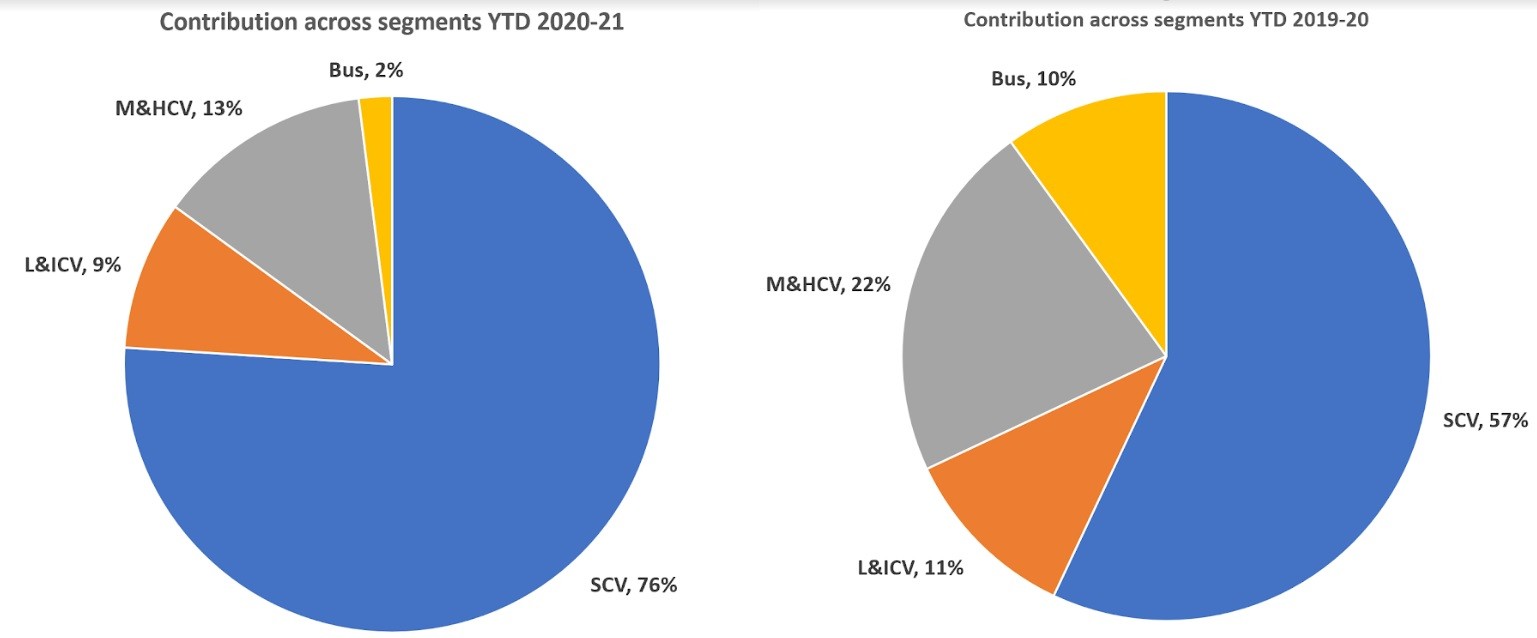

Hidden trend 1: Changing contribution across segments Year on Year

SCVs made up 57 percent of the CV industry volume YTD in 2019-20. However, in 2020-21, they make up a whopping 76 percent of the total volume. This is partly due to the fact that the SCV segment has seen a much faster recovery in comparison to other segments.

On the flip side, M&HCV and bus segment had the largest degrowth from 22 percent to 13 percent and 10 to 2 percent respectively. The L&ICV segment only de-grew slightly from 11 to 9 percent. The contributions from each segment remain largely similar for the month of September 2020.

SCV-Small Commercial Vehicles, L&ICV-Light & Intermediate Commercial Vehicles, M&HCVs-Medium & Heavy Commercial Vehicles, Bus: Passenger Vehicles

Hidden trend 2: Emerging importance of analysing industry segment performance

Commercial vehicle performance and NBFC performance focused primarily on the customer profile. Customers were profiled based on first time users or buyers, lower retail customers, upper retail customers and strategic customers. We believe that while this factor continues to be important, it is now critical to layer in the industry segment.

A handful of industry segments continue to drive volumes. Agriculture, rural demand and related transportation are driving SCV demand. Essential goods and FMCG products are driving demand for L&ICVs. E-commerce is driving demand for SCVs, ICVs and the 19-ton M&HCV trucks. Road contracts are driving demand for 10-wheel tippers. Industry sub-segments will continue to skew demand in H2 2020.

Major commercial vehicle segments

Hidden trend 3: Why not all excess capacity is available to satisfy demand? Why the CV industry will continue to grow despite overcapacity?

While there is significant excess capacity available in the market, not all capacity is easily transferable. For example, there is significant excess capacity in multi-axle HCVs. However, most of the industry sub-segment requirements are currently driven by SCVs, Single axle trucks and Tippers.

Similarly, there is significant overcapacity in Tippers carrying construction material and RMC vehicles. However, contractors who are completing road contracts are picking up new tippers. This is because these tippers are operated for 18 to 20 hours and need to be in excellent condition.

Most importantly, the demands of customers in each sub-segment are vastly different. We are seeing more specialization of operators in the Indian market for providing logistics similar to developed economies. This will also lead to the lower number of generalist operators that fall into the Market Load Operator (MLO) category. All these factors point to growth in sales of CVs in specific sub-segments despite overcapacity being available across the industry. There remains an arbitrage opportunity for some strong fleet operators who can leverage this excess capacity in alternate segments.

Hidden trend 4: Largely unchanged freight rates

Freight rates have largely remained unchanged. Rates today are largely the same as rates from Jan / Feb 2020. Since then, diesel prices have risen 15 – 20 percent. BS6 trucks cost over 20 – 25 percent more than similar BS4 trucks (for the equipment needed to meet stringent emission norms). Despite these challenges, rates for existing trucks and new trucks largely remain unchanged or have risen by less than 5 percent.

Customers picking up new trucks are anticipating running vehicles for up to 10 percent more kilometres per month in comparison to pre-Covid levels to offset these price increases. Hirers are also offering bonuses for limited periods of time like festival season running to keep operators engaged.

Segmental summary

In the section below, we briefly highlight the performance of the SCV, L&ICV, M&HCV and passenger sub-segments of commercial vehicles for September and H1 2020.

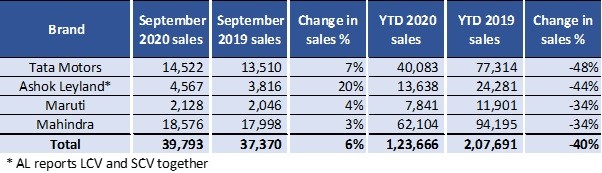

Small Commercial Vehicle (SCV) summary

Small Commercial Vehicle segment has performed well for the past 3 months. We anticipate that this trend will continue in H2 with a slew of new products being available. All major OEMs will continue to perform well in this segment. The YTD sales also ended with a drop of only 40 percent, the lowest among all CV sub-segments.

Light & Intermediate Commercial Vehicle (L&ICV) summary

The L&ICV segment should have a strong showing in H2 2020-21 making up for some of the lost volumes from H1. All major OEMs have performed well in this segment in September. Mahindra volumes are down only due to the non-availability of the Load king / Optimo tipper in BS6 for which trials are currently underway. The YTD drop was 64 percent, since the volumes were depressed until September 2020.

Medium & Heavy Commercial Vehicle (M&HCV) summary

M&HCV segment had a strong showing in September after a very challenging H1 2020-21. This segment has been driven by improved volumes in 10 wheel tippers and 19- tonne trucks which we anticipate will continue in H2. The year to date drop was 75 percent, driven by significantly low sales until August 2020.

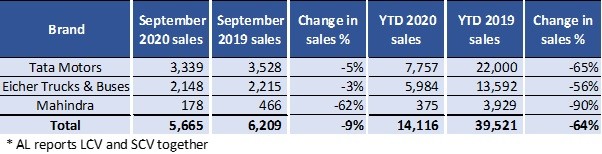

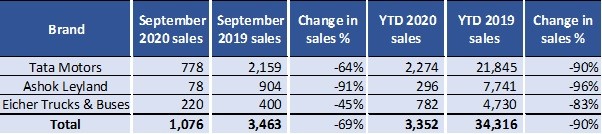

Passenger segment summary

Passenger transportation has been devastated by Covid 19. However, September offers us some hope of revival. While manufacturing firms have been driving demand for the limited number of buses being sold. The prospects for this segment will hinge largely on the actions taken by state governments to open up schools and inter-city travel. The YTD sales were down a whopping 90 percent.

The article was originally published in leaptrucks.com

| Kaushik Narayan is the chief executive officer & founder of Leaptrucks |

The views and opinions expressed in this article are those of the author and do not necessarily reflect the views of Indian Transport & Logistics News